rogerthat

Well-known member

- Joined

- Aug 29, 2015

- Messages

- 3,124

This is spot on. Lots of communities in this same boat. I think they are doing this to “subsidize” places with super high flood risk that should have never been built such as New OrleansI don't have a problem with the insurance, FEMA absolutely IS the problem and how they classified properties for the flood insurance requirement.

Does it make sense in NOLA yes, does it make sense in Laramie Wyoming when you have a creek that you can jump across anywhere, that's entrenched in a 30-40 foot cannel? Probably not, and in particular when the homes across the street (with more flood control in the streets) borders it are the ONLY homes paying for flood insurance. Never mind that if my rental house floods the people living behind me, as well as the University of Wyoming, are also going to be under the same amount of water.

I called FEMA directly and asked how they classified which homes need flood insurance and which ones don't. They had GIS analysts look at perennial water and made the determination arbitrarily on what they "thought" the risk of flooding was. I can tell you since that house was built in 1957, it has not come close to flooding. Further, I think their GIS analyst should try to get a basic understanding of elevation, noting that in some cases the houses that aren't required to have it on the next block over are LOWER in elevation than the houses that require it.

The unfortunate part, is many of the homes on that street are of the first time home buyer variety, in that 200-350K dollar range. That puts many of those homes out of reach when you have to factor in regular home owners insurance, plus flood insurance. Its a joke.

I painted FEMA's little red wagon and just cut a check to pay off the rental so we could drop the flood insurance and only paid one years premium.

Its a total scam in Laramie.

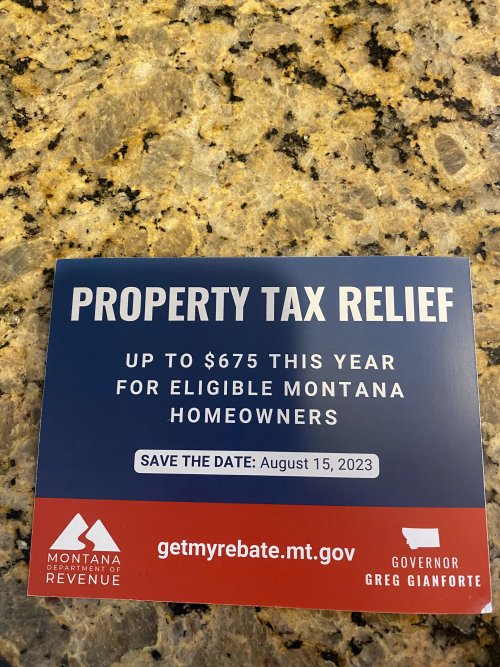

Pretty bold statement that won’t get him many friends in Helena.

Pretty bold statement that won’t get him many friends in Helena.